Can You Borrow and Lend USDC? Yes, You Can, Here’s How

Need a quick USDC without liquidating your existing crypto position? In this article, we will guide you on the basics of how to get a USDC loan—NFA article.

Lending and borrowing are the absolute cornerstones of the financial system, helping to create wealth and enable growth. Without them, the modern world simply wouldn't have been able to develop into what it is today.

Now, with the establishment of cryptocurrencies, the option is there for customers to use a whole new set of assets for lending and borrowing, and one of those is USDC.

But what exactly is USDC and how do you go about borrowing and lending it? Let's dig a little deeper to find out.

What is USDC?

USDC, or USD Coin to give it its full name, is a type of stablecoin that serves as a digital representation of the US dollar. It operates on a multi-chain infrastructure, primarily built on the Ethereum blockchain, but also compatible with other blockchains.

See USDC Stats on Coingecko: USDC Market Data

The purpose of USDC is to provide stable value in the notoriously volatile cryptocurrency market. With a 1:1 peg to the US dollar, each USDC token is backed by an equivalent amount of USD reserves held in audited bank accounts.

This means its value remains predictable, mitigating the aforementioned price volatility that plagues most other cryptocurrencies. In fact, since its creation in 2018, USDC has only ever suffered one depegging incident, triggered by the Silicon Valley bank crisis of March 2023.

It's also the second biggest stablecoin in the world by market capitalization, valued at just under $25 billion at time of writing, with only Tether boasting a higher value.

Read More: The Future of Real-World Asset Tokenization Explained (USDC is Often Used for Real-World Asset Investment)

The actual functionality of USDC relies on computer code known as smart contracts which allow for the issuance, transfer, and redemption of tokens. Thanks to seamless and real-time transactions on blockchain, USDC is a perfect candidate for peer-to-peer transactions, remittances, and payments.

Not only that, but USDC offers transparency and regulatory compliance by virtue of its strict adherence to established financial standards, undergoing regular verification of reserves backing the tokens.

This helps users feel confident in its stability and legitimacy. With all this in its locker, it's little wonder people see USDC as an attractive option for borrowing and lending in the cryptocurrency space.

Why would one take a USDC loan?

There are plenty of benefits to a USDC loan that makes it an attractive proposition for borrowers.

#1: Collateral Price Appreciation

One of the biggest upsides to USDC loans is the potential to benefit from price increases in the associated collateralized crypto assets.

When borrowers borrow USDC, they can use their crypto holdings as collateral, providing access to USDC liquidity without the need to sell those assets.

This allows them to both get their hands on USDC and maintain their exposure to the crypto market to potentially profit from future price increases – particularly useful during bull markets.

#2: Reinvesting Funds

Borrowing USDC also provides the opportunity to reinvest in high-growth assets. Rather than simply holding onto their collateralized crypto assets and hoping for the best, borrowers can use the borrowed USDC to invest in other promising crypto projects or decentralized finance opportunities.

This way, borrowers can diversify their holdings and max out their potential for returns by taking advantage of emerging trends and opportunities in the crypto market.

#3: Flexibility

USDC loans provide flexibility, with a variety of different repayment terms on offer. This allows borrowers to choose the particular loan period that best aligns with their financial goals and cash flow situation.

Thanks to this flexibility, individuals are able to take control of their finances and manage their borrowing and repayment schedule in a way that is most suited to their needs.

#4: Passive income potential

Borrowers have the opportunity to earn passive income from USDC loans by becoming lenders themselves.

Lending stablecoins like USDC on lending platforms or decentralized finance protocols can generate interest or yield, providing an additional income stream for borrowers.

This passive income is a real draw for anyone looking to make their assets work for them.

3 Easy Steps to Get a USDC Loan Now

Now we've talked through the benefits of taking out a USDC loan, maybe you're interested in obtaining one for yourself right now.

Luckily, we've outlined how to do this in three easy steps.

Follow these 3 steps to get a USDC loan:

#1: Prepare your collateral

Collateral usually plays a crucial role in the lending process, especially in the world of cryptocurrency. When you borrow or lend digital assets such as USDC, preparing collateral is usually the first port of call (more on that later).

It's a well-established method for mitigating risks to ensure a smooth and secure transaction.

Collateralization itself involves depositing a certain amount of crypto assets as security against the borrowed amount. This has several benefits for both lenders and borrowers alike.

From a lender's perspective, collateral reduces the risk of default as it serves as a buffer in case the borrower fails to repay the loan. In turn, thanks to this protection, borrowers benefit from more favorable interest rates when compared to unsecured loans.

In some cases, over-collateralization takes this a step further by requiring borrowers to provide a collateral amount greater than the value of the actual loan itself.

This added cushion may lead to even better interest rates for borrowers because the more collateral there is, the lower the chances of default.

This collateralization process helps establish trust between the two parties involved, and more broadly is one of the establishing principles in crypto lending to provide a secure and efficient alternative to traditional lending services.

#2: Find the Best USDC Lending Platform

Once your collateral is in place, it's time to find a USDC lending platform. One of the most important factors to consider during your search is the annual percentage yield (APY) on offer.

It's not all about the rate though, it's also important to take into account other factors like reputation, and the overall user experience a platform provides.

Make sure to execute due diligence by doing some comparison shopping and analyzing the features offered by the different platforms so you end up with the best USDC lending platform to suit your specific needs.

For a closer look at some of the options out there, we also included the top 3 USDC lending platforms later in the article.

#3: Remember your Loan Terms

When it comes to borrowing or lending USDC, always keep in mind the loan terms. These are likely to vary based on the lending platform and specific loan agreement you choose.

First up, pay attention to loan duration. Different lending platforms offer various loan periods, which could range from as little as a few days up to several months or even a year or more. Consider your financial goals and objectives to make sure you select the term most appropriate to you.

Another crucial factor is the associated interest rates. Again, different lending platforms will offer different interest rates, and it's important to compare and contrast to ensure the platform you choose is competitive. Higher interest rates maximize your earnings, after all.

Lastly, bear in mind the collateral requirements. Some lending platforms may require you to provide collateral in the form of other digital assets to secure your loan. Ensure you understand exactly what is involved as well as the associated risks.

While we're on the subject of risks, a quick reminder that you should always have a proper handle on the risks involved when borrowing USDC. Market risks, including price volatility of USDC and other crypto assets, should be considered, as should other risks like smart contract risk, counterparty risk, and regulatory risk.

Stay informed and choose a lending platform that aligns with your financial goals and risk profile.

Top 3 USDC Lending Platforms

In this section, we'll explore three of the top USDC lending platforms out there to help you make informed decisions in the decentralized finance space.

Read More: How to Invest in DeFi in 2023

Whether you are a crypto enthusiast looking for additional yield or seeking to borrow stablecoins, these platforms offer a secure and efficient way to participate in the world of decentralized lending.

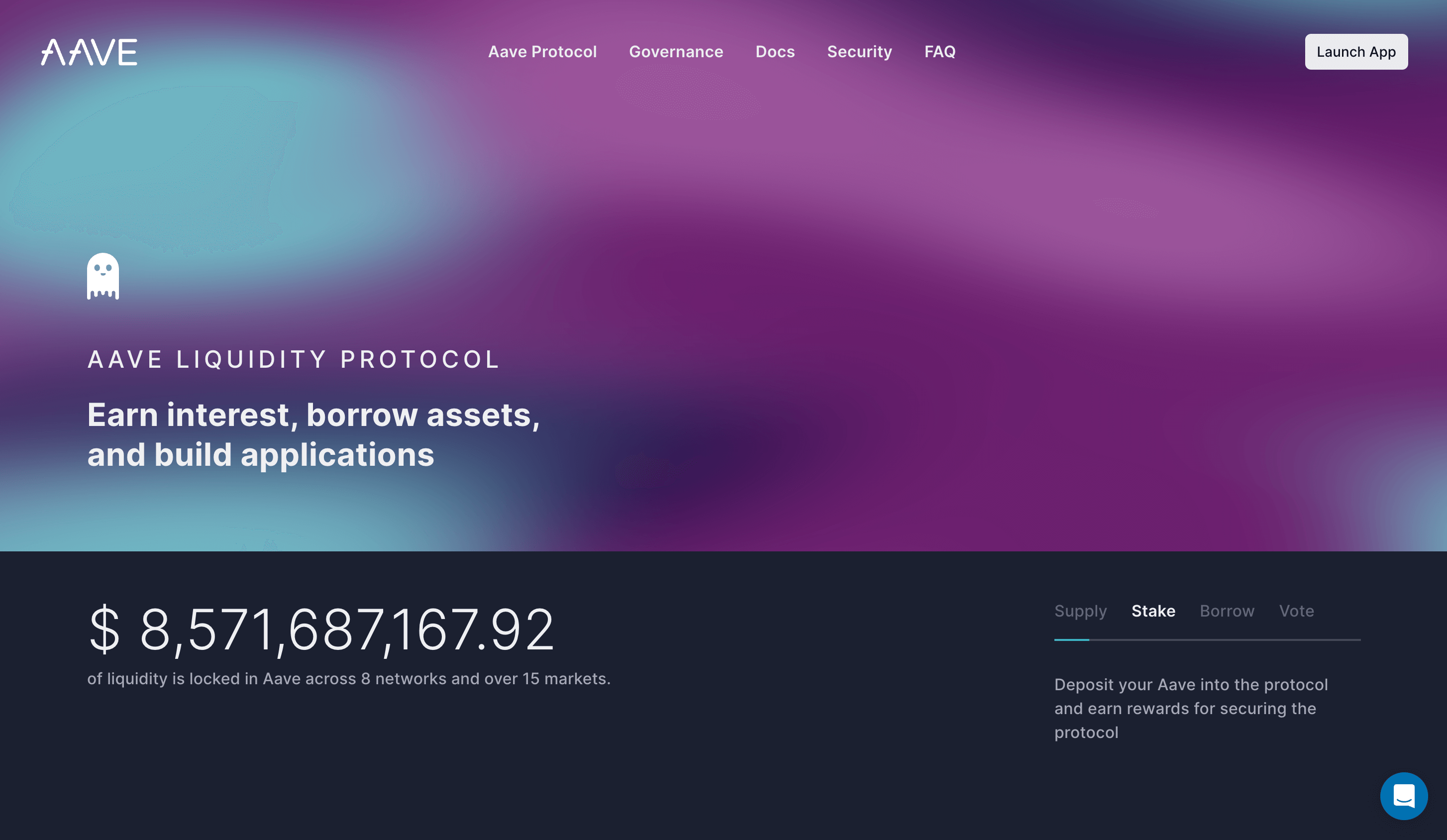

#1: Aave

Aave is a prominent decentralized finance (DeFi) market that offers a wide range of lending services to crypto users. Although there is a diverse range of digital assets available for lending, USDC is one of the most prominent assets on the platform.

One of the key factors that make Aave an attractive platform for lending USDC is its competitive interest rate. Aave employs a unique interest rate model known as a "money market protocol," which ensures fair and dynamic interest rates based on supply and demand.

This means that as more users lend their USDC on the platform, the interest rates for providing liquidity may increase, allowing lenders to earn a higher return on their assets.

Leveraging the Aave platform, users can seamlessly earn passive income by lending their USDC tokens to borrowers while enjoying the security and transparency provided by the blockchain and smart contract technology. Although, of course, like any lending, Aave involves potential risks, including market volatility and the risk of default by borrowers.

Aave does, however, strive to mitigate these risks through implementing measures like liquidation options and lending limits.

With its competitive interest rates and innovative lending services, Aave is definitely a platform for those seeking to lend or borrow USDC to consider.

Website: https://aave.com/

#2: Compound

Compound is a leading decentralized lending platform with a long history and a well-established reputation. To get started, users simply need to connect their Ethereum wallet to the Compound platform at app.compound.finance.

Borrowers can borrow USDC by supplying an approved collateral asset. This collateral acts as security for the loan and helps maintain stability on the platform. Borrowers need to monitor their collateral value and maintain a sufficient collateralization ratio to avoid the risk of liquidation.

For those looking to lend USDC, they can deposit their tokens into the platform and receive cUSDC in return. This represents their lending position, and the interest accrues over time in their account. Lenders can withdraw their USDC at any time by redeeming their cUSDC.

Like Aave, Compound utilizes smart contracts to ensure transparency and security throughout the lending and borrowing process. Users have full control over their funds through their Ethereum wallet, and transactions occur directly on the blockchain.

Compound allows you to participate in the lending and borrowing of USDC, earning interest as lenders or accessing liquidity as borrowers. It provides a convenient and decentralized solution for those seeking to leverage their assets and access additional capital.

Website: https://compound.finance/

#3: NEXO

Nexo is a popular USDC lending platform that offers attractive features for users looking to earn passive income. With Nexo, lenders can enjoy a double-figure Annual Percentage Yield (APY) on their USDC deposits, making it an appealing option for those seeking to grow their wealth.

Read More: CeFi vs DeFi: What's the Difference?

One key advantage of Nexo is its user-friendly interface, making it accessible for beginners who are new to the world of crypto lending. The platform provides a seamless and intuitive experience, allowing users to easily deposit their USDC and start earning interest right away.

Additionally, Nexo offers perks for using their native token, NEXO. By holding NEXO tokens, users can earn higher interest rates on their USDC deposits. This incentivizes users to engage with the platform and maximize their earnings potential.

Nexo stands out by providing compound daily payouts and flexible earnings, allowing users to withdraw their earnings at any time without any fees or penalties. What's more, Nexo offers insurance coverage for custodial assets, providing an extra layer of security and peace of mind for users.

However, it's important to note that Nexo no longer accepts customers from the United States for regulatory reasons. Despite this limitation, Nexo remains a reliable and reputable USDC lending platform for users around the world.

Website: https://nexo.com/borrow

Collateralized vs Non-Collateralized Lending

So far, we've been talking in terms of collateralized loans only, but in the world of cryptocurrency lending, there are actually two main types of lending: collateralized and non-collateralized.

#1: Collateralized loans

As we've discussed, collateralized lending requires borrowers to provide crypto assets as collateral upfront to secure the loan, in the form of Bitcoin or Ethereum, for example.

This collateralization acts as a demonstration of commitment on the part of the borrower to pay back the loan and protects lenders against default.

Advantages and Disadvantages of Collateralized Loans

Advantage:

- Interest Rates: Lower interest rates due to reduced lender risk.

- Loan Amount: Access to larger loan amounts compared to non-collateralized loans.

Disadvantages:

- Collateral Requirement: Borrowers must have sufficient collateral, which can be prohibitive for some.

- Financial Inclusion: Limits financial inclusion, particularly in non-traditional financial systems.

- Overcollateralization: In overcollateralized lending, the loan amount is often less than the value of the collateral, which might not be efficient or advantageous for the borrower.

Non-Collateralized Loans

On the other hand, non-collateralized lending has no such requirement for borrowers to provide any crypto assets as collateral.

Lenders instead evaluate borrowers based on their creditworthiness and reputation within the crypto community, or on an increasingly rich array of data sources through the use of machine learning technology.

Advantages and Disadvantages of Non-Collateralized Loans

Advantages:

- Flexibility for Borrowers: Offers more flexibility for borrowers without sufficient crypto assets to use as collateral.

- Interest Rates: Historically higher, but innovations in risk assessment are leading to potentially lower rates.

- Risk Assessment: Innovations in risk assessment are improving the viability and appeal of non-collateralized loans.

- Crypto Asset Requirement: No need for crypto assets as collateral, making it more accessible to a broader range of borrowers.

Disadvantages:

- Interest Rates: Historically higher rates to compensate for increased lender risk.

How About Lending instead of Borrowing? Here's Examples of Non-Collateralized USDC Lending

While non-collateralized lending is rarer than collateralized lending, there are opportunities out there.

Read More: Direct Lending vs Private Credit in Cryptocurrency

Many of them exist in areas where collateralized lending is particularly prohibitive, such as emerging markets, and focus on allowing businesses and individuals to grow and thrive in the real world rather than propping up recursive crypto investments.

#1: Jenfi via Gluwa (Expired)

For digital businesses looking to borrow USDC in Asia to fund marketing and growth campaigns without the need for traditional collateral, Jenfi in collaboration with Gluwa is one option.

The lending process through Jenfi is simple and user-friendly. Borrowers can easily access USDC loans by submitting a loan request and receiving a reply within 24hrs. Once funds are distributed, repayment happens through a percentage of revenue model based on what the business generates. Lenders looking to invest their USDC in Jenfi can expose their assets to the company through the Gluwa platform, who then lend out the funds.

One of the key benefits of Jenfi's partnership with Gluwa is the reduced risk exposure for lenders. While traditional lending platforms require collateral to mitigate risk, Jenfi's non-collateralized lending approach shifts the risk to the borrower, providing lenders with additional security.

Jenfi's collaboration with Gluwa offers a unique way to enact non-collateralized USDC lending that benefits the borrower while also offering investors the chance to earn returns by stumping up funds to help improve financial inclusion.

#2: Fazz via Goldfinch (Locked)

Fazz via Goldfinch is a non-collateralized lending platform that offers a revolutionary approach to borrowing and lending USDC. Unlike traditional lending platforms, Fazz does not require borrowers to provide collateral to obtain a loan.

This opens up lending opportunities for individuals who may not have access to valuable assets for collateralization.

The unique feature of Fazz via Goldfinch lies in its credit underwriting process. Instead of relying solely on collateral, Fazz assesses each borrower's creditworthiness based on various factors such as income, repayment history, and financial behavior. This allows Fazz to offer loans to a wider range of borrowers, including those who may not possess significant assets for collateral.

To further enhance trust and mitigate risk, Fazz via Goldfinch also incorporates a mechanism called social proof. Borrowers can onboard a co-signer with a strong credit profile to increase their chances of loan approval and obtain more favorable terms.

This innovative platform not only provides a convenient way for individuals to access much-needed funds but also offers an opportunity for lenders to earn passive income through lending their USDC tokens. With Fazz via Goldfinch, borrowers can unlock financial opportunities without being hindered by the requirement for collateral, while lenders can diversify their investment portfolio by participating in the lending process.

Plenty of Ways to Get Involved in Borrowing or Lending USDC

Borrowing and lending with USDC is a rich and varied landscape. Both businesses and individuals alike can benefit, whether that's to use it as an additional income stream as a lender, or even to grow a digital startup business as a borrower.

With all this just an internet connection away, it's no surprise that people are talking about the benefits.

If and how you decide to get involved in the space comes down to your particular needs and goals.

Toby Bromet

Toby Bromet Benedict Clark

Benedict Clark