Bullish Trends in Africa's Emerging Crypto Landscape

Is the exponential growth of crypto adoption finished or are we just getting started?

Digital Asset Adoption

Crypto assets have emerged as a transformative force in the global financial landscape since the introduction of Bitcoin by Satoshi Nakamoto in 2008. Initially a niche interest, crypto ownership has surged from five million in 2016 to over 516 million by 2023, alongside the diversification of the market to include over 9,000 different tokens according to Statista. Nowhere has this rapid evolution been more impactful than in Africa, a continent traditionally underserved by conventional financial systems.

Roughly 40% of the African continent’s population is 15 or younger, and demographically constitutes 27% of the world’s population. Forecasts call for Africa’s digital economy to grow as much as 600% by 2050.

The economic outlook across the continent looks set for quick expansion, with growth expected at roughly 3.7 percent in 2024 and 4.3 percent in 2025. With countries like Nigeria and South Africa at the forefront, the adoption of crypto (and other high-tech innovation) has been happening at breakneck speeds.

This research report explores the dynamics driving Africa's burgeoning crypto landscape, arguing that the continent's unique demographic, economic, and technological conditions position it as a potential epicenter for future crypto development. As Africa continues to gain ground economically and demand for more efficient remittance systems grows, the continent is quickly reconciling widely acknowledged digital and connectivity gaps.

Demonstrating a Keen Interest

As mentioned, interest in digital assets on the continent has exploded in recent years, and it’s now home to the two most crypto-aware nations on the planet, with South Africa and Nigeria leading the way. What’s more, Africa also plays host to the most crypto-curious country in the world. Analyzing Google searches involving ‘invest in crypto’ and ‘buy crypto’ worldwide, it’s not the likes of the U.S. that top the list, but Nigeria. It’s also not the only African representative either, Kenya also makes it onto the list in 15th place.

Interest levels aren’t evenly spread across the continent, however. Thanks to a combination of Nigeria’s massive population and high interest, paired with the contribution of other countries in the region such as Ghana and Ivory Coast, it’s West Africa that ranks as the regional hub, claiming the lion's share with 74.7% of interest. Northern Africa (10.0%) Southern Africa (9.6%). East Africa (3.8%) and Central Africa (1.9%) are all nations with significant room for growth.

Rapid Upswing in Engagement

It’s not just interest that’s rife in Africa, but users are actively transacting on-chain. According to Chainalysis—a measure that takes into account a variety of factors including De-Fi, P2P, and centralized exchange value—African countries accounted for eight of the top 40 places on the list in 2023: Nigeria (2), Morocco (20), Kenya (21), Tanzania (24), Ghana (29) South Africa (31), Egypt (35) and Ethiopia (36).

Africa is now home to some of the countries with the highest levels of crypto ownership and use in the world. Once again, Nigeria is top of the global tree—a massive 35% of Nigerians aged between 18 and 60 owned crypto assets or had traded them in 2022. and as much as 47% of the population aged between 18-64 has used crypto before. South Africa (22%), Egypt (19%), and Morocco (16%) all feature in the top 20 as well.

According to KuCoin’s Into the Cryptoverse Report, roughly 52% of Nigerian crypto investors allocated over half of their assets to crypto back in 2022. Also, 65% of Nigerian crypto investors on-ramped fiat deposits to crypto or stablecoins via OTC trading. Another important finding was that 70% of Nigerian crypto investors planned to increase their crypto positions over the next 6 months, suggesting that adoption in the country has been accelerating for some time.

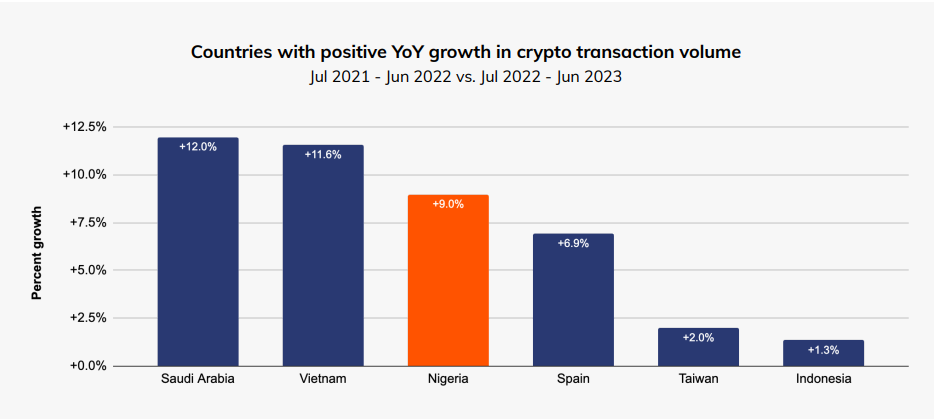

Even in the face of the recent worldwide bear market, Nigeria has been flying the crypto flag. Transactions in the country grew 9% between 2022 to 2023—a figure that puts it third globally in terms of growth. In fact, Nigeria was one of only six countries in the top 50 by size whose crypto transaction volume grew year-over-year in that period.

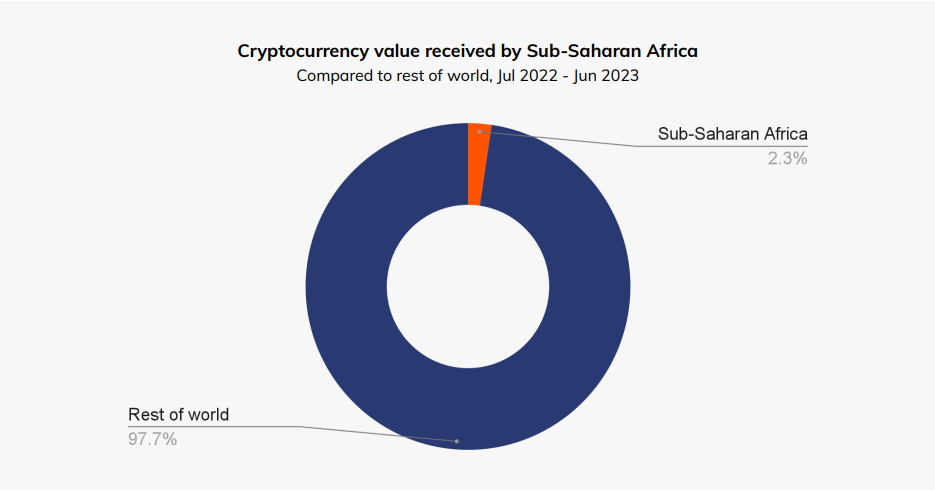

However, while Africa boasts some of the fastest growing crypto markets anywhere on earth, the overall value of the market remains small in global terms. Sub-saharan Africa, for example, made up just 2.3% of crypto value received from mid-2022 to mid-2023.

This does, however, leave ample room for future growth, and if trends continue in the same direction as in recent years then there’s every reason to predict explosive growth.

Popular Crypto Assets

Different regions show different preferences when it comes to specific crypto assets users have been inquiring about online.

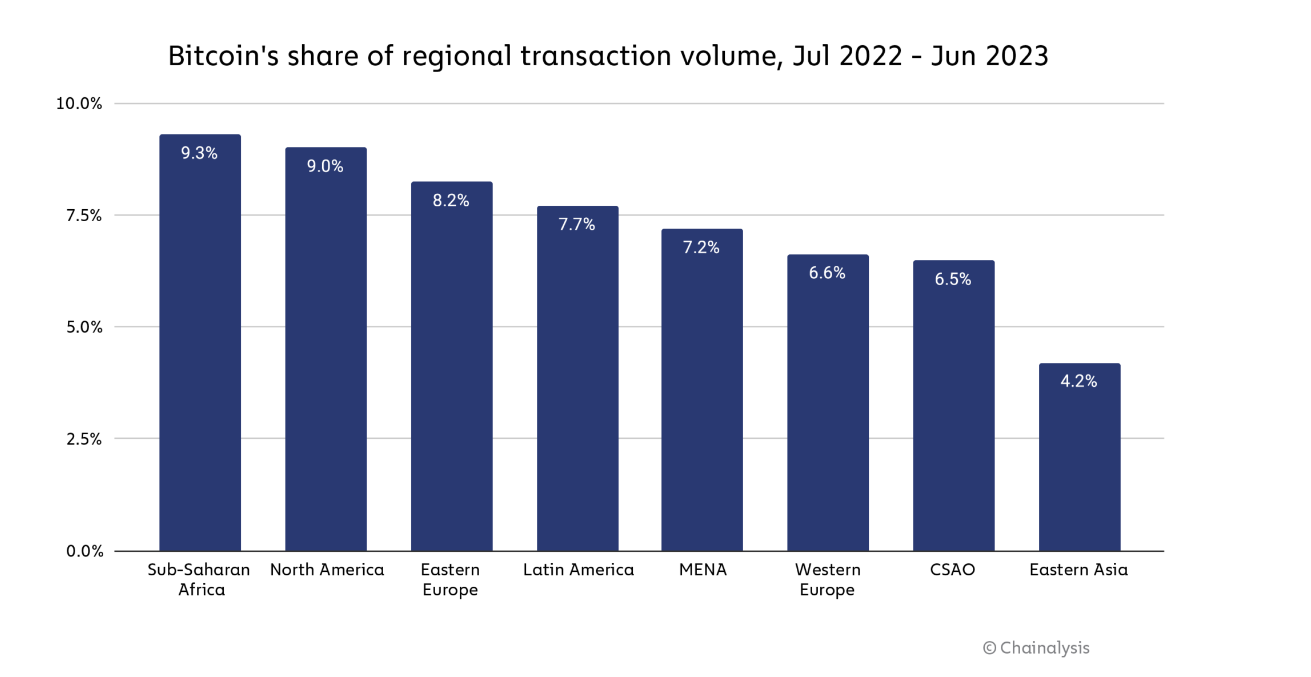

Though altcoins are high up on the list for search results, when it comes down to transactions it’s Bitcoin that tops the list. No other region on Earth has a higher percentage of crypto transactions made up from Bitcoin than sub-Saharan Africa at 9.3%.

Venture Funding in Blockchain

All this growth is now being reflected in the VC landscape, too. According to a 2022 report, African blockchain enterprises raised $474 million. Compared to the relatively paltry $90 million raised the previous year, this represents a sizable jump of 429% (massively outpacing general VC funding which increased by only 34%) and equates to the biggest increase of any region—although this figure still pales in comparison to the $15.3 billion raised in the U.S.

As might be expected given its dominance in previous measures, Nigeria (13) led the way in terms of sheer number of deals, followed by South Africa (4) and Seychelles (3). However, due to a relatively low average deal size of $1.25 million, it was in fact the Seychelles and South Africa, not Nigeria, that accounted for the overwhelming majority of actual funds raised (81%).

This is largely a reflection of the fact that Seychelles, alongside Mauritius, has become a favored destination for global blockchain firms in Africa thanks to favorable business-oriented policies. The tiny island nation is even home to the first African blockchain unicorns — crypto exchange Kucoin and EVM-compatible zk-rollup project Scroll.io — claiming the fabled status in Q3 2022 and Q1 2023 respectively.

Africa recorded a 429% surge in blockchain funding across 2022.

What’s Driving Crypto’s Rise in Africa?

That the crypto space in Africa has made such strides forward is no coincidence, a number of factors have come together in recent years to create the kind of conditions favorable to growth.

Demographics

For starters, Africa has a very young population. Especially sub-Saharan Africa, which has the youngest population of any area in the world — 70% of people being under the age of 30 according to the UN. The younger generation are naturally more tech-curious and tech-savvy than their older counterparts, and feel far more confident engaging with technologies like crypto, further accelerating adoption.

Economic Conditions

Although it’s by no means alone in this regard, the theme of rising inflation and debt has been depressingly common across Africa in recent years, particularly in the wake of the COVID-19 pandemic. High inflation has been hitting ordinary Africans in the pocket, in the short-term decreasing their purchasing power, and in the medium to long-term putting their savings at risk.

A quick look at the African nations featured on the Global Crypto Adoption list reveals a clear correlation with countries battling difficult economic headwinds. Ghana, for instance, experienced inflation of over 50% in 2023, while South Africa saw official unemployment rates rise as high as 30%.

Meanwhile, number two on the list, Nigeria, has been dogged by persistent economic problems of its own. In the last decade, Nigeria has suffered major recessions with the collapse of oil prices, not to mention multiple Naira devaluation incidents set to the backdrop of inflation at nearly 30%.

All this economic turmoil has forced Africans to seek alternative ways to store value, maintain purchasing power and undertake financial transactions. While those fortunate enough to exist in more stable economic circumstances may balk at the prospect of relying on crypto to do this given their notorious volatility, in extreme economic conditions, needs must. Even so, perhaps with this volatility in mind, and in the face of the market downturn of recent years, Africans have increasingly looked to stablecoins, a more reliable store of value thanks to their fiat currency pegs.

Beyond acting as a store of value, crypto also offers alternative ways to generate income, critical in countries facing the kind of unemployment rates of South Africa. Rewards from proof of stake consensus mechanisms, finding airdrops and giveaways, and even generating income through play-to-earn games all provide potential sources of income.

Remittances

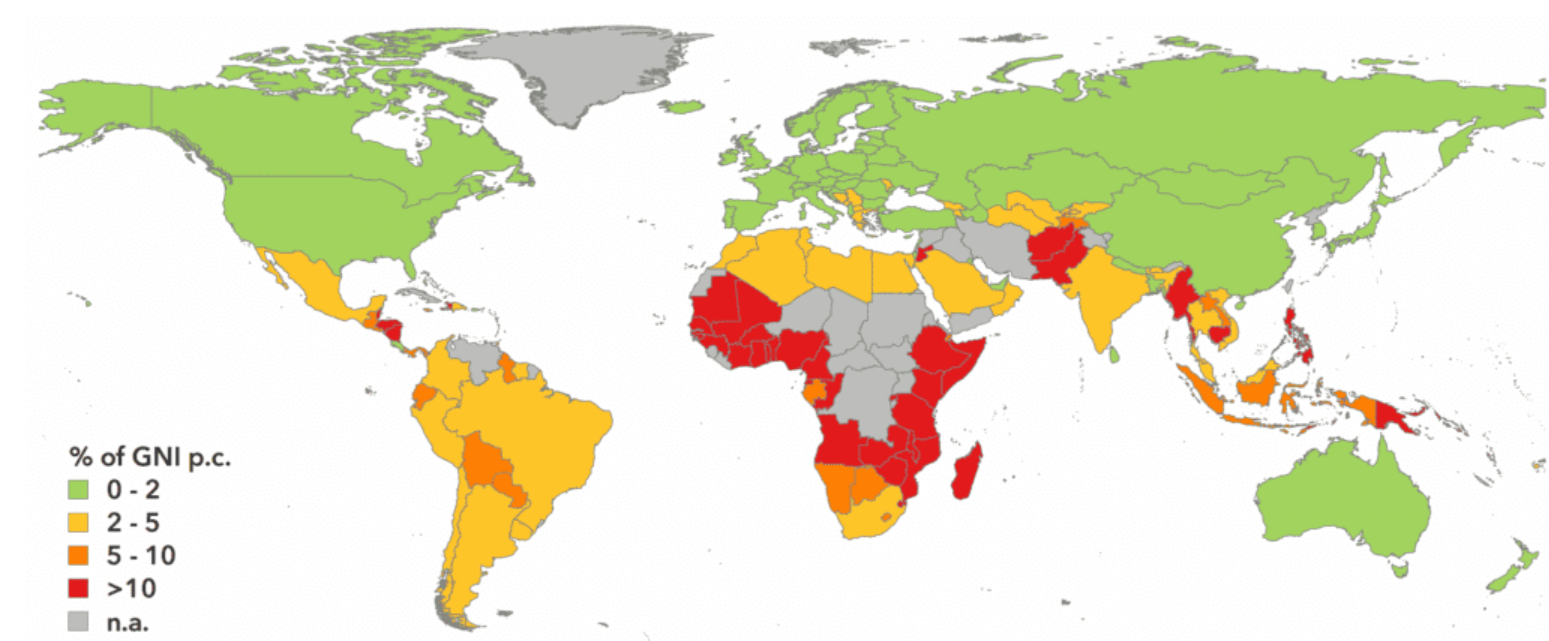

The continent racks up around $50 billion in remittance payments every year, a figure that is constantly rising thanks to increased migration. Nigeria, which accounts for 38% of remittance flows to the region, saw these flows grow by about 2% across 2023, while two other major crypto spots, Ghana and Kenya, posted estimated gains of 5.6% and 3.8%, respectively.

For many years, the likes of Western Union and MoneyGram have been tapping into this trend to make millions in profits by charging Africans high fees. Now the development of crypto and other smart contract primitives has given Africans an alternative solution to send money both regionally and globally, bypassing these traditional, and often significantly costlier, money transfer services. Given more than 88.5% of crypto transactions made by Africans are cross-border transfers, it seems as if users are keen to capitalize.

Financial Inclusion

The fact Africans are turning to crypto in such numbers is also a reflection of a failing traditional financial system. Even in this modern world, there are 1.4 billion people across the globe who don’t have access to a bank account—a significant proportion of those are in Africa. Due to a mix of factors including colonial legacies, civil wars, and rugged terrains, Africa has historically suffered from a poor traditional financial infrastructure, contributing to issues with financial exclusion.

“Financial inclusion is defined as the availability and equality of access to financial services regardless of personal net worth or company size”—Boston Consulting Group

While in 2021, the average rate of account ownership in developing economies had increased from 63% up to 71%, only around 55% of sub-saharan Africans and 48% of North Africans aged 15 and over are financial account holders, with some sources showing upwards of 65% of adults across sub-Saharan Africa unbanked.

This is a big problem. Exclusion from financial services makes it much more difficult to manage and save money, or access credit. This in turn holds people back from improving their financial situation and serves to reinforce existing problems around social exclusion, poverty, and inequality.

Lack of money, distance to the nearest financial institution, and insufficient documentation are consistently cited by unbanked adults as some of the primary reasons they do not have an account.

How Technology Can Help

Now technology is starting to provide solutions. In recent years, Africa has been undergoing a digital finance revolution that’s helping to bring financial products to those who need them most.

Tech in Action: Mobile Money

M-Pesa is an apt demonstration of how financial inclusion can be improved through technological innovation. Back in 2007, Kenyan mobile network operator Safaricom (affiliated with Vodafone) saw that its customers were using prepaid airtime as a form of currency. Inspired by this, Safaricom developed the M-Pesa mobile money solution— a name in reference to the word ‘money’ in Swahili—allowing users to send each other money through SMS.

First, users KYC and register for an M-Pesa account and are issued a SIM card by authorized M-Pesa agents. To deposit money into their M-Pesa account, users visit an M-Pesa agent. The agent takes the cash and credits the equivalent amount to the user’s M-Pesa account. Withdrawals work the same in reverse.

For transfers and payments, users enter the recipient's M-Pesa phone number and the amount to be transferred. M-Pesa also allows users to pay for goods and services, utility bills, and more directly using their mobile account. M-Pesa also offers savings accounts, loans, and international remittances.

Mobile money has proven to be incredibly successful and has since spread to other countries including Tanzania, Mozambique, DRC, Lesotho, Ghana, Egypt, Afghanistan, South Africa and Ethiopia. Crypto adoption is the next logical step in this regard towards individuals in Africa tapping into broader financial networks, not to mention remote employment opportunities worldwide.

Crypto’s Role in Financial Inclusion

Thanks to the particular qualities they possess, crypto is uniquely positioned to address issues around financial inclusion.

Borderless

The fact that DeFi is borderless is a huge advantage for a continent where the global and regional movement of value between people is vital. The blockchain networks that power crypto assets are agnostic to geographical location, meaning users are freed of many of the fees, rules, and restrictions that hamper cross-border transactions in traditional finance.

Permissionless

One of the main prerequisites for gaining access to traditional financial services is proof of identity. On a continent where at last count an estimated 500 million lacked official identification, accessing lines of credit or bootstrapping a startup presents significant challenges, not to mention the standard banking services many take for granted. The permissionless nature of blockchain means that anyone with an internet connection can generate a wallet address and begin to transact P2P, therefore bypassing the issue via the power of DeFi, collateralized lending, stablecoins, and more.

Accessible

Participating in DeFi requires nothing more than an internet connection. This makes the technology especially practical in Africa where there are many isolated and underserved areas with little to no availability of standard banking services. In many cases, physical banks are simply too cumbersome for a commute either in terms of time and money spent, or the opportunity cost of taking time off from work.

Decentralized

Centralized bodies—such as the aforementioned remittance companies—charge sizable transaction fees when funds are moved or spent in traditional financial services. Ultimately, this means services are either unfeasible or people are forced to give up a high proportion of their hard-earned wages. With DeFi, there is no need for intermediaries, reducing unnecessary transaction fees.

Secure

Thanks to the blind justice of neutral smart contracts, private-key encryption, and strict collateralization requirements, crypto is arguably more secure than traditional banking systems. With countries such as Nigeria (42%), Kenya (42%) and South Africa (29%) registering trust in governmental institutions levels significantly below global averages, a decentralized and securely encrypted currency free of the control and manipulation of institutions is an attractive prospect.

Barriers to Overcome

Of course, crypto is no magic bullet. A number of structural challenges must be overcome if Africa is to realize the full benefit of crypto.

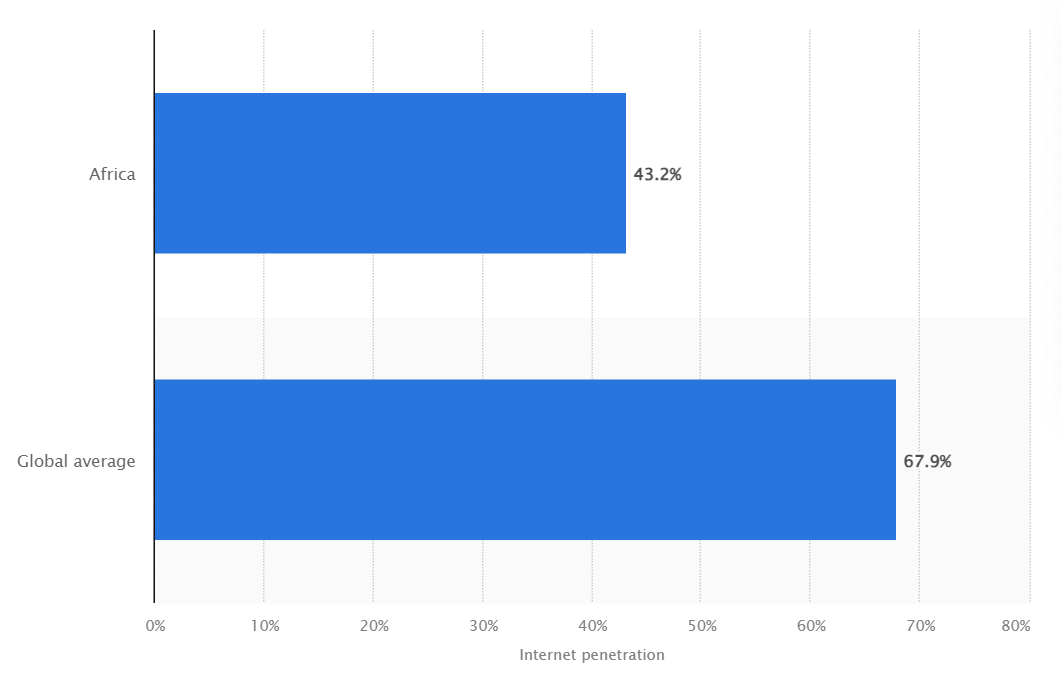

Internet Access

Something often touted as a key advantage of crypto is that the only prerequisite for participating is internet access. However, that also means Africans without internet access are left out in the cold. This is a significant problem on a continent where internet penetration rates sit far below the global average:

Connecting the continent is a monumental undertaking, not to mention an extremely expensive one—the cost of bringing broadband to the whole of Africa by 2030 has been estimated at $100 billion.

Yet there are reasons to be optimistic. Back in 2010, penetration rates in Africa were as low as 9.6% in some areas, and in 2000, internet access was almost non-existent. There has already been a significant improvement.

Not only that, but mobile broadband coverage via 3G and 4G networks has been rapidly expanding—available to 82% of the population in Africa even back in 2021, (49% for 4G and 33% for 3G)—and 5G networks are now being rolled out across a number of different countries.

Perhaps as much as anything, the problem is one of data affordability. In 2021, Africans had to pay, on average, 6.5% of their monthly income for 2GB of mobile data—barely enough to watch four hours of low-quality video on Netflix. Users in Asia-Pacific, by contrast, were only paying 1.7%, and Europeans just 0.5%. Affordability of broadband connectivity is the lowest across Africa—fixed broadband being less affordable than mobile.

Internet connections simply must become more physically and financially available to Africans if crypto is to be successfully brought to the masses.

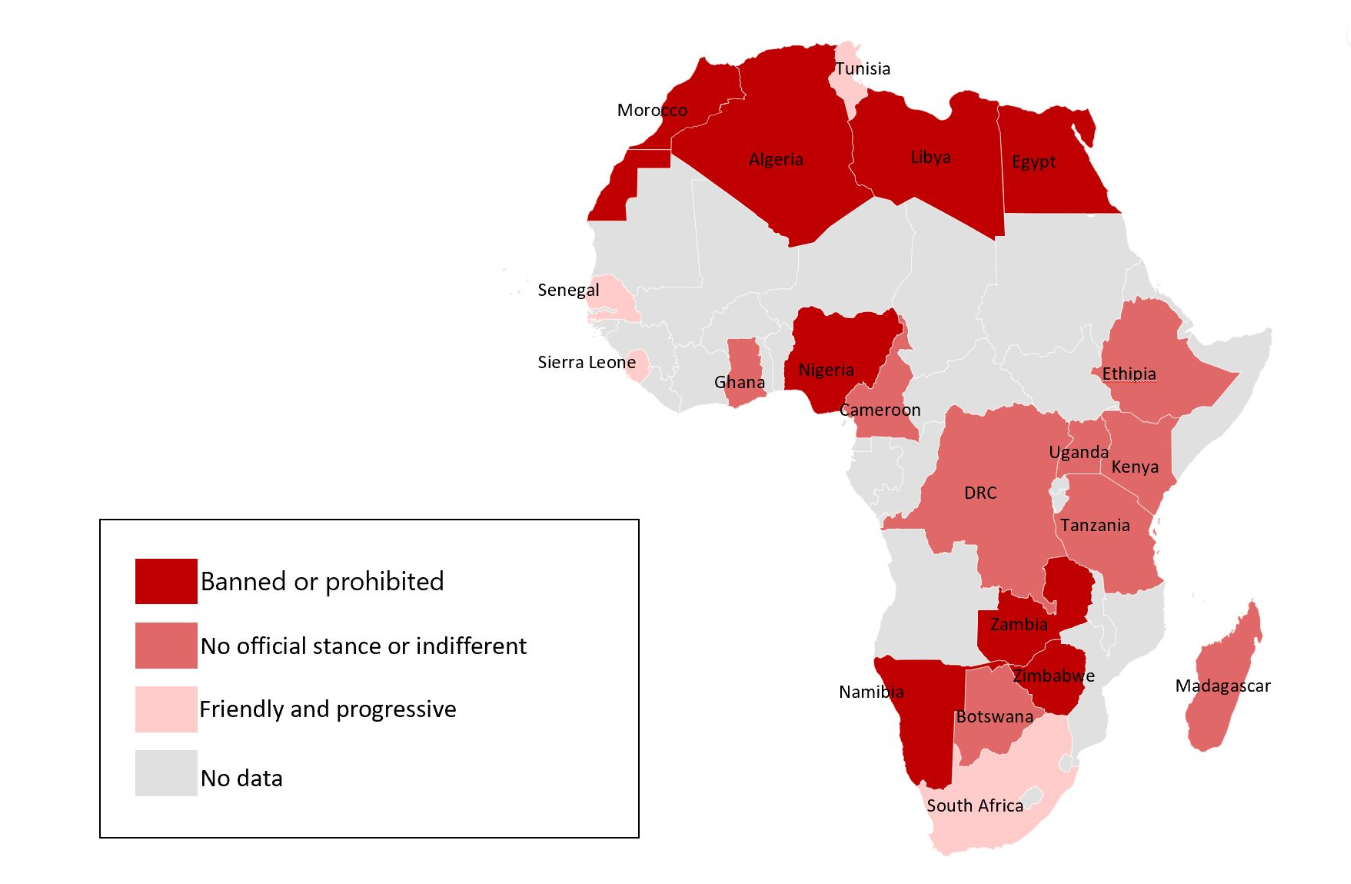

Regulations

Crypto regulation in Africa varies greatly from region to region, both in terms of its exact status and in terms of the proactivity national governments have demonstrated in crafting and implementing legislation.

One of the forerunners in this regard is South Africa. At the end of 2022, the Financial Sector Conduct Authority (FSCA) officially categorized crypto assets as financial products and announced a licensing regime for crypto businesses, in one fell swoop providing legal clarity as well as scope for financial investigators to fight illicit activity.

Other countries have made notable strides forward. In 2023, Kenya introduced The Capital Markets (Amendment) Bill, categorizing crypto assets as securities and introducing a framework for levying capital gains tax on crypto assets stored in both digital wallets and crypto exchanges.

Once again, proponents hailed the legal clarity this brings, and pointed to the ability of these measures to safeguard the economy from financial crimes. Over in the Central African Republic, the government had its own ‘El Salvador moment’ by declaring Bitcoin a legal tender in April 2022. Crypto users naturally flocked to peer-to-peer trading platforms, a sector in which Nigeria still leads the world.

“Current trends globally have shown that there is a need to regulate the activities of virtual assets service providers which include cryptocurrencies and crypto assets,”—Central Bank of Nigeria.

The explosive demand for digital assets and P2P marketplaces demonstrates the peoples’ desire to engage with DeFi across the continent, opening up conversations regarding what might be achieved with an even more supportive regulatory environment.

Still, greater regulation raises problems of its own. Particularly where KYC and AML checks are put in place that rely on identification documentation, something many Africans lack. Leaders need to strike the right balance between accessibility and protection to make sure incentives are structured so as to allow for growth while at the same time safeguarding against financial malfeasance.

Crypto Education

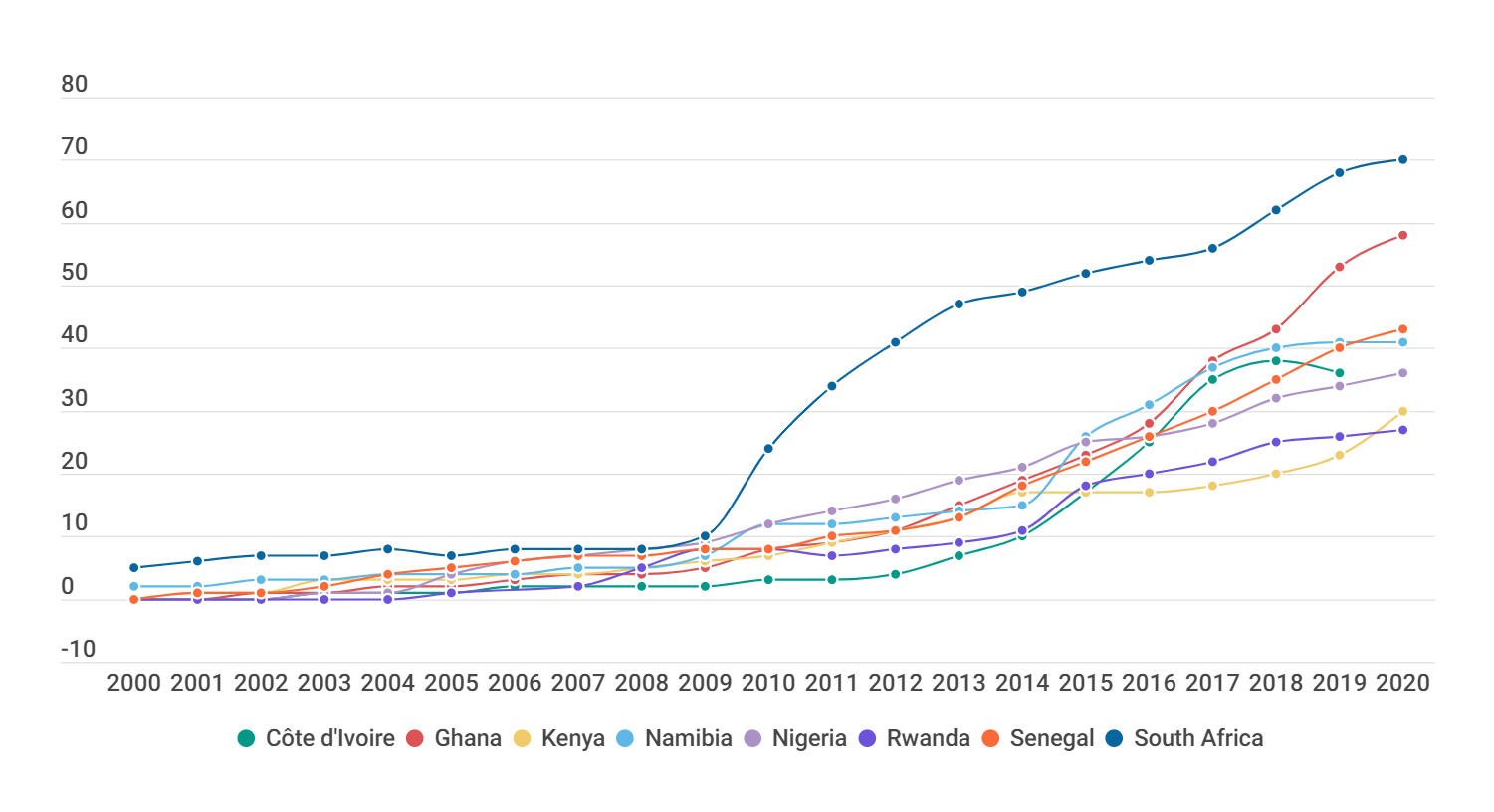

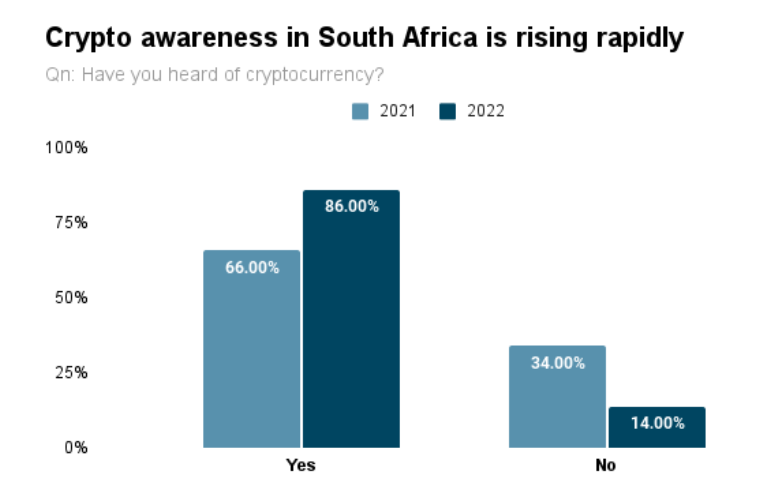

If people are to effectively engage with crypto and reap its benefits, they need a real understanding of what it is and how it works. In South Africa, one of the most progressive and friendly environments for crypto in Africa, crypto awareness rose from 66% to 86% between 2021 and 2022, and the general sentiment is very positive, associating crypto with the future of money and digital ownership.

In some cases, crypto companies have taken on the burden of education themselves. The Binance Masterclass program, which provides crypto education ranging from trading to career opportunities in blockchain, launched in January 2020 with the aim of increasing crypto literacy in Africa and had already provided education to more than 400,000 users by the end of 2021. Empowering people in this way opens doors, equipping learners with the tools to harness the benefits of crypto and navigate an ever-evolving financial landscape.

Still, more must be done, and the remit must be extended to include the likes of vendors. As things stand, crypto is far from universally accepted as a form of payment. This means utilizing crypto’s value often still involves converting funds into fiat currency, something that frequently relies on a bank account, creating a significant barrier in crypto’s fight for financial inclusion.

Looking to the Future

Other regions may buy and sell more crypto than Africa right now, but no other area has a greater day-to-day need for it. Driven by the quest for financial freedom, even in the face of significant challenges, digital assets are already altering the economic landscape on the continent.

Projections show Africa’s population will double from current levels to 2.6 billion by 2050, at which point a quarter of the world’s population, and one in three youths globally will be of the African continent. This puts it in a unique position for the mass adoption of digital assets in the future.

Given the still relatively nascent state of the crypto industry, there is a huge opportunity unfolding for Africa here. Tackle the issues in its way, and there's a continent rich in energy and spirit ready to embrace digital ownership and set Africa on the fast track to the cutting edge of the technological financial world.

Creditcoin Takes Action

Creditcoin was launched in 2019 to help people and companies access lines of credit by connecting them via blockchain to local lenders, acting as an open, transparent, and decentralized credit bureau. The protocol established a public ledger for recording loan performance on-chain, thus facilitating a shared record of publicly verifiable credit histories and giving Creditcoin users access to yield-bearing real-world assets.

Partnering with local fintech lenders, like Aella in Nigeria, Creditcoin has been providing a secure and decentralized environment for users to build their credit reputations, access the liquidity they need, and on increasingly more favorable terms. Creditcoin has already partnered with global financial service providers to record over 5M credit transactions on-chain.

In furthering financial inclusion on the continent, Creditcoin’s development company, Gluwa, has made significant strides by partnering with the Central Bank of Nigeria to facilitate the development and adoption of its CBDC, the eNaira.

References

- AFDB. African economic outlook 2024. African Development Bank Group.

- Consensys. (2023). The state of web3 perception around the world. Consensys Reports.

- Greaves, G. (2022). The African blockchain report. CV VC.

- Hruby, A. (2023). Critical connectivity: Reducing the price of data in African markets. Atlantic Council.

- Ng, J. (2023). Top 15 countries most curious about cryptocurrency. CoinGecko.

- Qian, L. Y. (2023). Crypto interest in Africa still nascent. CoinGecko.

About Creditcoin

Creditcoin is the world’s leading real-world asset infrastructure chain for financial institutions, connecting global borrowers, lenders and investors on-chain. To date, the protocol has helped its partners record over 4.27 million real-world credit transactions, valued at $79.7 million USD, while servicing 337,000 customers worldwide across emerging markets.

By transparently securing credit history and loan performance on the Creditcoin network, the protocol has already helped thousands of borrowers, businesses, and investors secure capital financing, build credit history, and grow their global RWA investment footprint.

Website | Twitter | Discord | Medium | Youtube | Telegram(ANN) | Whitepaper | Credit Penguin Colony (Opensea)